It’s been about two months since the Lahaina fire, and the long term nature of their recovery is just starting to set in — for some at least. I know from first-hand experience that it takes months for some people to emerge enough from the fog of trauma to even start thinking about recovery.

Personally, I don’t like the word “recovery”.

It makes it sound like things can — and do — go back to the way they were before the fire (or the hurricane or the flood — pick your own mass climate disaster).

But they don’t. They can’t. Lahaina is gone. Forever.

Sure, something will come back — probably cookie-cutter multi-million dollar condos that the former residents can’t even dream of affording. But Lahaina is gone. Its residents can move forward, but they can’t “recover”. There is no going back.

And “moving forward” itself a long and cruelly painful process, and one during which I personally came to understand that the “system” — everything from FEMA to insurance companies to the tax system to banks to the government to the legal system — isn’t designed to help you, the disaster victim.

It isn’t that the system doesn’t work. It works exactly as designed.

But it’s just not designed to help you.

It helps others, or maybe no one at all, but if you manage to get what you need from the system, it’s almost by accident, or unintentional, or a byproduct of helping someone else.

I know a lot of people reading this will say, “you’re overreacting” or “you just had a bad experience”. I know that because I’ve been told this before by people who have never been through a climate disaster and who are just repeating the reassuring platitudes that we’re all programmed to repeat.

I mean, we have to trust the system, right? The system isn’t based on a lie, right? The moment we grasp that the system isn’t designed to benefit us, then the legitimacy of the system comes into question. And for a “functioning” society, we cannot have that.

But I’m not some left-wing radical socialist in a Che Guevara T-shirt. I’m not even really mad at the system. I just learned how the system really works. I don’t like it. But I accept it as a fact.

So, yes, repeat all the platitudes back to me. I would be saying them myself if I never had to experience how the system works first-hand.

But I did.

This is not to say that people in the system were trying to screw us personally. No. Many were very nice. But they were working in the system and for the system, and even though they may have wanted to help, the system wasn’t really designed to make that fully possible.

If I were to detail all the ways — big and small — that the system screws climate victims, this article would be a book. So I’ll try not to do that.

And the ways that the system screws victims are boring and mundane and stupid and greedy and pointless.

Not exactly fodder for gripping reading, and I apologize for that in advance. But if you stick with me, you will definitely learn something. I sure as hell did.

(At the very least, read the section on the legal system. If that doesn’t convince you, nothing will.)

But let’s start with banks. Everybody loves banks!

Banks

There are a thousand different ways that banks screw you, intentionally or otherwise. It is, after all, one of the things they do best. But let’s just talk about the one biggest way that they screw disaster victims.

About a month after the Camp Fire, we got a letter from our mortgage holder, a small, not particularly efficient bank based in the San Francisco Bay area. It had come to their attention that the “collateral” on our mortgage had recently undergone a radical devaluation, and they wanted us to pay off our mortgage.

All of it. NOW. A check would be fine, thank you very much.

What? You were under the illusion that somehow you weren’t going to be responsible for paying the full price for a pile of toxic ashes?

Well, banks exist to make money, and this is standard practice.

If you don’t pay your mortgage, banks foreclose and take your home. Homes are worth money. So the banking system is designed to do okay no matter whether you pay or not. Your money or your house. Simple.

But once the house is gone, they lose the ability to make money if you don’t pay, so they want you to pay now. And they will use threats and lawyers to make sure you do pay for that pile of toxic ash, whether you have the money to do that or not. That’s what the system is designed to do.

Lost your home, your job, your town? Sucks to be you. But the system is designed to insure that the banks profit, not to help you “recover” — or even make it possible to “recover”.

But we were “lucky”. We had homeowners insurance. Our house was worth $350,000 — according to them. No problem to rebuild — according to them. Too bad that half of the money you’re going to need to rebuild has to go to pay off that toxic ash pile. C’est la vie!

Oh, and don’t think we were ever even given the opportunity to not pay off that mortgage. Oh no. The check from our insurer was made out to us AND the bank. We had to send it to them before we could get a penny, and they definitely took their full share before sending the remains along to us.

You, the victim? You’re not first in line. That’s the way the system is designed.

Is that wrong? That’s not my point. My point is that it hurts, not helps, victims. That’s all. Whether the system should hurt victims is a separate question.

Insurance

Insurance. Ah, insurance!

According to my therapist, I still have PTSD from dealing with our insurer. Not from nearly dying in the fire mind you; from dealing with our insurer after the fire. That’s how traumatic the experience was.

You may not be aware, but after a mass disaster, all the major insurers send big semis full of adjusters to the site of the disaster. There were vans from Nationwide, State Farm, Allstate, AAA, and several others after the Camp Fire.

They generally start off great. They practically force a check for $5,000 on you. “For expenses. You’ll need it.” Wow, nice!

Then, “You have this much coverage and you’ll get every penny of it,” they say as they slide a calculator with what seems to be a very large number on it in your direction.

It seems like a lot of money, but there are several invisible asterisks attached to it. They don’t tell you about them the day after the fire. But very quickly, you start to become aware of them.

First of all, that amount is your structure coverage (Coverage A), plus something called “Extended Replacement Cost” (ERC). It’s typically set at 50% of Coverage A. So, in our case, we had $363,300 in Coverage A, plus &181,650 in ERC. ERC is an extra amount “available” to you in case rebuilding your home costs more than your Coverage A.

Bored yet? The asterisks will make it more interesting.

*Depending on the state, ERC is ONLY available if you rebuild onsite. So, if, say, your entire town is wiped out and you have no choice but to relocate, this money isn’t available to you. In California, the law says they must give you this money regardless of whether you rebuild or relocate, but our insurer could not have cared less about California law. We’ve never seen a penny of it, and never will.

*Aside from the ERC, your Coverage A is a maximum amount. Your insurer is absolutely going to send out an appraiser to appraise the value of your home as of the day before the disaster. If they low-ball the appraisal, you will only get what they say your house was worth, even if that’s less than the the amount of your coverage or the cost to replace it.

*Remember the bank? Right, those guys! They get their share of your insurance before you see a penny.

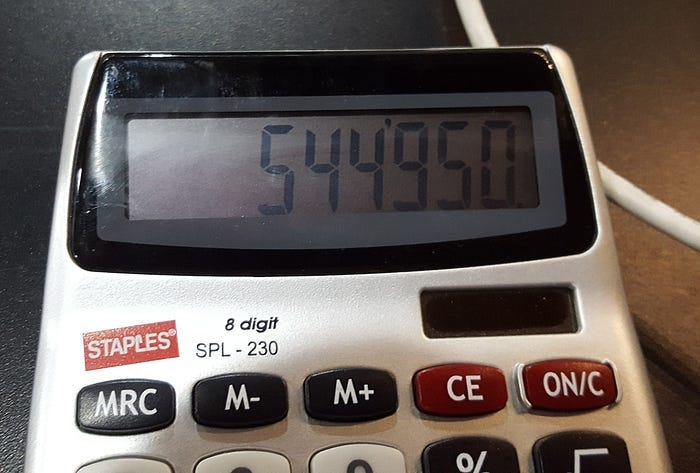

So let’s take that $544,950 and see what we actually got to “recover”:

+$544,950: “Total Coverage”

-$181,650: ERC denied by insurer despite state law

-$13,300: Low-ball house appraisal

-$178,573: Remaining balance on mortgage

$171,427

Even 5 years ago you couldn’t buy an outhouse in California for that amount of money.

We didn’t “just have a bad experience”. Though not everyone went through this, many did, and many more will as insurers put the screws to policyholders in order to maintain profits and shareholder dividends.

The system is designed to insure that insurers profit, not for you to even have a chance to “recover”.

Is that wrong? I don’t have the answer to that. But I do know that insurance — despite all the “good hands” and “good neighbor” and “on your side” marketing crap — isn’t really there to help you as much as you probably think.

But even if we had gotten every single penny of insurance and our bank had forgiven our mortgage out of hearts bursting with compassion, would that $544,950 have been enough to rebuild?

Not by half.

After the fire, there was a frenzy, not only of people trying to rebuild, but also of fraud, as fake contractors moved in to con victims. So it took us a while, but we finally found a reliable contractor who was willing to do a full estimate for a reasonable price (unlike the guy who wanted to charge us $18,000 for an estimate).

One million bucks plus. Supply and demand, baby. Contractors were in short supply. Materials were in high demand. The economic system was working as designed. It just wasn’t helping us.

Seen enough yet? No? A glutton for punishment, you are.

Okay, then, let’s talk contents! As part of your insurance policy, you have a section called “Personal Property” or Coverage C. Most people just call it “contents”, because it represents coverage for the contents of your home. It’s typically 60–75% of your structure coverage.

Different insurers handle contents payouts differently. Some just give you a flat percent of your home value. Maybe fair. Maybe not. But simple. Easy.

Ours violated the Geneva Convention.

We were required to account for every single fork, toothpick, and pair of underwear we owned.

No, I’m not kidding. I have a spreadsheet with 6,221 items in it, inventorying every single thing we could remember. Books? Better list every one by title and value. Condiments? How many different kinds of mustard did you really have? Exactly how many cans of Campbell’s Tomato Soup were in the back of the cupboard?

Of course, you can’t remember everything. No one really expects you to. Your insurer sure doesn’t want you to. But we tried. Three years after the fire, we were still remembering things. “Is that on the list?” we’d ask each other. A living nightmare.

Does that sound like a system designed to help you?

So, you have to remember everything you owned and put a value on it. And then your insurer takes that list and depreciates everything by up to 80%. Why? Because they can. That’s how the system is designed.

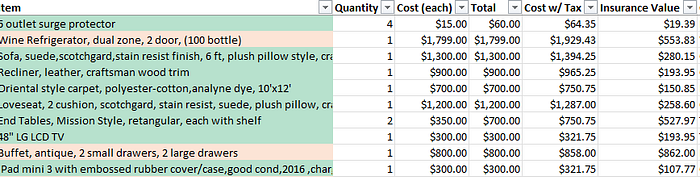

Here’s a snippet from my spreadsheet. The replacement cost for just the items listed was $8,643.28. The amount given to us by our insurance was only $3,148.46, only 36% of the cost to replace those items.

In the end, when we finally gave up trying to remember more lost things, we figured that we had $277,595 worth of stuff. With depreciation, our insurer gave us $190,000.

The system worked as designed.

FEMA

We were, by all accounts, lucky. We didn’t have to deal with FEMA. Actually, we weren’t allowed to because we had insurance. FEMA only helps people without insurance. Who knew?

But we still had to apply for FEMA aid because (little known fact!) without a FEMA case number, you don’t qualify for all kinds of things. No SBA loans, no low-interest disaster declaration loans, no extensions on your insurance, no access to relief funds… whole bunch of things. A very important number.

But that was the extent of our experience with FEMA. So, I don’t have any personal horror stories about dealing with FEMA.

But I do know that after the Camp Fire, the line of people trying to apply for FEMA aid literally went around the block.

And I also know that even though 14,000 homes were destroyed in the Camp Fire, it was 6 months before FEMA got even one trailer in place. Nine months after the fire, just over 200 FEMA trailers were in place. Way too little, way too late.

And, of course, they ended up closing those trailers and kicking out the remaining residents, who had literally nowhere else to go.

By all accounts, FEMA is a nightmare to deal with. My wife and I were both educators with three Master’s degrees between us, and the paperwork was mind boggling. Imagine being an under-educated person or an elderly person with mild dementia and trying to navigate the labyrinth of Federal paperwork requirements. How is that helping?

And what if you had lost your ID and Social Security card in the fire? It could take weeks to replace them, and without them, no FEMA aid.

I’m not actually sure who FEMA is designed to benefit. Maybe nobody. Or maybe the bottom line with FEMA is that it’s just an underfunded bureaucratic shitshow with a very poorly defined purpose and goals. The people in FEMA may be well-intentioned, but they are clearly overworked, underfunded, and mired in red tape.

The Government

The government, whether state or federal, doesn’t really care about you. That’s my conclusion. It’s not that it is necessarily trying to hurt you; it mostly just wants to pretend that you don’t exist.

Case in point. Remember how our insurer totally ignored California state law with regards to paying Extended Replacement Cost (ERC)?

Well, we took that directly to the California Department of Insurance.

Their mission statement seems pretty clear:

The California Department of Insurance is the consumer protection agency for the nation’s largest insurance marketplace and safeguards all of the state’s consumers by fairly regulating the insurance industry. Under the Commissioner’s direction, the Department uses its authority to protect Californians from insurance rates that are excessive, inadequate, or unfairly discriminatory, oversee insurer solvency to pay claims, set standards for agents and broker licensing, perform market conduct reviews of insurance companies, resolve consumer complaints, and investigate and prosecute insurance fraud.

They showed Nationwide who was who, right?

Not exactly. The most we ever got out of them was a sternly worded letter to Nationwide asking them to obey state law. Seriously. All they did was send them a letter asking them to comply with the law. Toothless is hardly the word.

In all fairness, like FEMA they were understaffed and underfunded. After a mass event like the Camp Fire, they were inundated with complaints.

But still, that was how the Department of Insurance was designed. Not helpful to us in any way.

I won’t even get into the pictures of Insurance Commissioner Ricardo Lara partying with insurance company CEOs, because I’m sure that was totally fine.

The Legal System

I left the legal system for last because it deserves to burn in a very special, very exclusive hell.

Two months after the Camp Fire, when it was becoming clear that PG&E (the nation’s largest investor-owned utility) had caused the fire that had killed 85 people and left 40,000 people homeless, PG&E declared bankruptcy.

Bankruptcy protects you from your creditors, and PG&E had just created 40,000 brand new creditors. How’s that system working? As designed.

But here’s where the system broke down a bit. There was so much anger among the public toward PG&E that there was a lot of pressure to do something, even though PG&E had legally said “NOT IT!”.

So the first thing they (PG&E, the state, and the bankruptcy court) did was… pay the insurance companies $11 billion for their “losses”.

Not us. Pfft. We only lost our lives, our homes, and our town.

The insurance companies were the REAL victims (if you buy that, I have a bunch of bridges to sell you). At the very least, they had better lobbyists.

The fact is that insurance companies actually have insurance. It’s called reinsurance. Look it up. And even if they didn’t have reinsurance, they could write off any payouts as a loss on their taxes.

But whatever.The fun part of all that was that after they paid off the insurance companies there wasn’t enough money left to pay off the actual fire victims. Oops!

So the genius plan they (same folks, plus a bunch of lawyers) came up with was to pay us half in cash, and half in PG&E stock!

Yeah, sure, I want to own a piece of the company that tried to kill me. I want this company to burn in hell and pay for it’s crimes, but I also have to hope it’s stock goes up so I don’t end up living in the street??

Seems… I dunno, a bit conflicting.

As you can imagine, this was a wildly popular decision (again, I got bridges for sale) that we had really no voice in.

Yes, technically, we were given a choice, but that choice was essentially “bend over and get screwed repeatedly, plus some cash eventually” or “probably get nothing ever”.

That’s really not that far off from how our lawyers actually sold it to us (they may have left out the bend over part).

We certainly had no voice in coming up with this insane deal. We were just forced to swallow it.

And of course the lawyers wanted us to take the “plus some cash” option. They stood to make billions if we said yes. And of course, not knowing any better, we all did.

At this point (mid-2020) the crazy was just getting started.

I could spend a week going over the insane ins and outs of the PG&E settlement. It’s really stupid and cruel. But let me just lay out where the money from the settlement ends up.

So, let’s say — after nearly 5 years — you get a “determination” of your claim from the trust set up to administer the funds from the settlement. Let’s say that determination is a cool million dollars, which to be honest, is pretty close to our claim.

$1,000,000. Su-weet!

By now, you should be cluing into the fact that you, the disaster victim, are not going to see most of that money. Somebody will, but it won’t be you.

And before we even get to the breakdown, let me state that this is how the settlement system was literally designed to function. None of this was really hidden from us, but neither was it spelled out in black and white.

So first of all, remember how the insurance companies had an $11 billion party at PG&E’s expense, leaving not enough money for the actual fire victims?

Yeah, well, turns out that the money left (including that stock) is only enough to pay 60% of claims.

So there’s $400,000 gone right there. Poof.

But you were smart. You hired one of the many a̶m̶b̶u̶l̶a̶n̶c̶e̶ ̶c̶h̶a̶s̶e̶r̶s law firms that swarmed fire victims, promising to “maximize your settlement!!”. Good for you!

We actually waited to nearly the last minute and went with a local Paradise lawyer who had lost his home in the fire. But he was quickly overwhelmed by the complexity of the case and ended up joining forces with one of the largest tort firms in the country.

(Their senior partner, does take the time to do periodic “town halls” with fire victims.But he likes to say that he had to leave other commitments and fly on a Sunday morning to Chico from Texas in his private jet just to meet with fire victims. This doesn’t go over as quite the sacrifice that he seems to think it is… to people still living in leaky RVs four years after the fire.)

And this fancy-dancy law firm has more than once completely borked our claim. One time, when they were getting things repeatedly wrong, I asked them to send us every document they had from us on our claim, and they sent me hundreds of sensitive documents from other people’s claims! Again, I’m not making this up. Oh, I got calls from all the partners and their lawyers on that one (mostly to insure that I wasn’t going to “make a big deal” out of it).

Anyway, regardless of how incompetent they are, the lawyers get one third of the settlement right off the top.

They make a very big deal about all of the firms they’ve brought in to t̶a̶k̶e̶ ̶o̶u̶r̶ ̶m̶o̶n̶e̶y maximize our settlement. There’s the company that cuts the checks (and charges $375 per check for the privilege). There’s the company that… well I forget them all now, but at one point I counted 14 separate companies hired by our lawyers to do SOMETHING VERY IMPORTANT. They all get a nice cut of our settlement.

So, anyway, one third of $600,000 is $200,000.

$400,000 left.

That leaves taxes. And guess what?!? Our lawyers fees — that $200,000 — is taxable! Even though we never see it. Yep, that’s actually true. Our lawyers have said so much. The IRS has confirmed it.

So we get taxed on $600,000, even though we only see $400,000. Given about 20% state and federal taxes, that’s $120,000. California passed a law exempting settlements from state taxes, but we don’t live in California any more. So, so much for that.

Let’s do a little more math:

+1,000,000: Total settlement “determination”

-$400,000: That PG&E doesn’t have to pay

-$200,000: In lawyer’s fees

-$120,000: In taxes

$280,000

Out of a million dollar settlement, we actually get only $280,000. That was how the system was designed to work. And, as a side note, we haven’t actually seen any of that $280,000 yet. Maybe by the 5th anniversary of the fire!

Adding that $280,000 to the $171,427 we got from our insurance equals not near enough to rebuild.Only about $600,000 short. Soooo close!

What Was Possible

In a system designed to actually do everything possible to help victims, things might have looked a bit different.

Why should I have to pay for a house that no longer exists? Fuck the bank. They have insurance. I need that money for a new home.

$178,573

Why shouldn’t insurers be forced to abide by state law, and give me everything I paid for in my policy premium?

$194,950

Why shouldn’t be compensated for the actual cost to replace all the contents I lost, not just what some insurance company thinks it’s worth after depreciation?

$87,595

Why the hell am I paying a bunch of incompetent lawyers and their associated parasites to constantly screw up my claim? How many times do I have to fix their mistakes before I’m the one being paid??

$200,000

And why the goddamned hell does a corporation — one that killed 85 people, destroyed an entire town, and made 40,000 people homeless and traumatized — get to keep 40% of everyone’s claim?What the actual fuck???

$400,000

Money isn’t everything, but when you’ve lost everything, the only way to “recover” is via money. That’s how our system is designed to work.

In a system that was designed to actually put victims first and prioritize their recovery ahead of corporate profits, we would have had an extra $1,061,118 in our pockets to help us recover.

Maybe that’s too much. I won’t argue the point. I’m not greedy. (It actually seems like a lot! I never did the math before. Fuckers.)

And I know this isn’t how our system works (boy howdy, do I!), but that’s not to say that our system — or someone’s system in a better world — couldn’t be designed to work this way.

But as more and more people experience climate change and become victims of climate disasters, we’re going to have to do something.

Maybe that something is sacrifice billions of people to homelessness so that a few corporate billionaires can continue to live la dolce vita on their yachts and private jets.

Maybe. Or maybe it’s time to realize that you could be next, and that you might want to live in a system designed to support and help you when the bad shit comes and you have no choice but to try to rebuild your life.

Maybe.